August 2015 Imtech shareholders get ZERO, a permanent loss of capital. Jeroen Brenninkmeijer of http://www.mjradvies.nl/ was right about not buying Imtech after the first bad news appeared.

Here my previous posts on Imtech.

Imtech a possible BUY at around €10

|

| Old chart February 1st 2013 |

Imtech 2012 numbers were expected February 5th, now they are delayed.

2011 Imtech Graham screen: FAILED in CURRENT RATIO and LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS. Which is the reason they are now in trouble with the banks after a major loss in Poland.

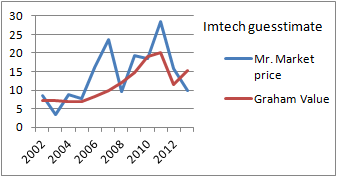

Book value 2011 was €932m/87,5m shares is €10,6 per share. The loss in Poland is at least €100million. Too be safe, we'll make it 232m. Guesstimate book value per share = €700/€87,5 = €8,-

New lower EPS estimate for 2013 €1,30 (was €1,7 in 2011). €0,- for 2012.

Guesstimate of Graham value: Graham number of √(22,5 x €1,3 EPS x €8 Book Value/per share) = €15,2

|

| Imtech guesstimate with 232 million Polish write off and 0.- profit in 2012 (February 4th, 2013) |

No comments:

Post a Comment