After around 2 decades of working on an issue that has puzzled many retailers especially colleagues at C&A (and the founder and planning department at IKEA for at least 10 years), I am moving on to a new chapter in life.

Insight

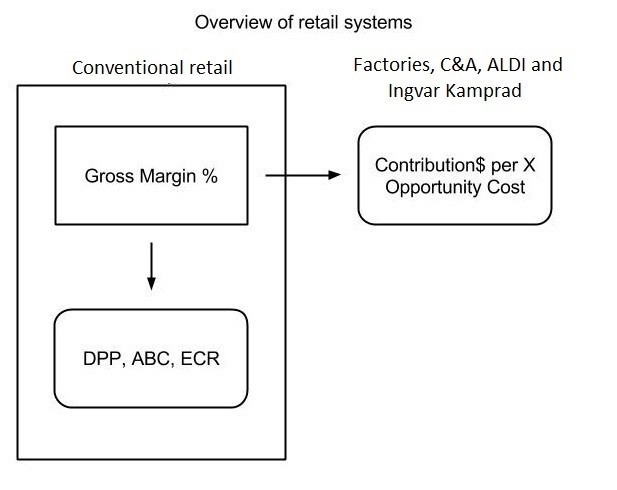

The insight was that you could make a higher Return on Equity in retail partly as result of having much lower Gross Margin percentages than your competitors. (Gross margin is referred to as “Buyers Calculated Profit” (BCP%) at C&A).

The cutting in half of the BCP% at C&A to just 25% in 1906 led to what the Brenninkmeijers called a Snowball effect. After decades of uphill struggle, making money became relatively easy. The C&A “Sneeuwbal System” is very similar to the Walton family’s “Productivity Loop” and what Jeff Bezos of Amazon, refers to as the “Flywheel of Growth”.

Information

Throughout the twentieth century, C&A colleagues shipped boxes of detailed sales information from the stores by car and truck to datacenters every day, long before the IT and barcode revolution reached other retailers. By quickly knowing on a weekly basis exactly which items (styles) were selling, profitable decisions could be made 52 times a year. This led to a fast fashion advantage with a constant flow of new designs driven by real-time customer demand. Competitors, on the other hand, who only knew what had been sold once or twice a year when they counted inventory, were left in the dust.

An added advantage of C&A’s information edge was that Opportunity Costs and contribution dollars could be directly calculated at style level as is customary in every industry except retail. For other retailers, this was impossible because they only tracked the total daily sales amount and an estimated average gross margin percentage. In contrast to C&A, they had no idea what they were actually selling in real time.

Garbage in, garbage out

In the last years of the twentieth century, C&A somehow adopted the sub-optimal planning, pricing and evaluation systems of competitors who used average gross margin percentage targets. This led to a false belief at C&A that gross margin percentages needed to be increased above 50% to remain profitable, even-though new entrants were successful with much lower BCP%s. This led to lower sales, losses, and layoffs at C&A. I have put it down to the original framework being “lost in translation” when C&A merged the European country companies and the operating language was switched from German to English. Retail communication can be confusing in English. You might say “This low margin style creates a high margin.” which is a lot more clear in German “This low “Handelspanne %” style generates a high “Deckkungsbeitrag $”.

At IKEA, the founder Ingvar Kamprad asked his planning department: “What the hell are percentages anyway?” Ingvar owned factories using dollar contribution and tracked sales at style (SKU) level so he couldn’t understand why somebody would make decisions based on gross margin % targets. The answer to his question is that a gross margin percentage is a sub-optimal workaround only used because long ago most retailers lacked Information Systems.

Opportunity Cost? That is the question!

If you don’t base merchandising decisions on gross margin or average operating expense percentages, the obvious question would seem to be: “What are the actual costs involved in selling articles and how do I allocate them?”

When I asked my uncle who was CEO of C&A Global between 1960 and 1988 about this, he replied that I was asking the wrong question. “Small differences in operating expense are much less relevant than substantial Opportunity Costs incurred when choosing to sell a low dollar contribution (BCP Fund €) option instead of something that generates more contribution dollars. The question is: “What is the Opportunity Cost of choosing option A instead of option B?” See Opportunitätskosten : https://de.wikipedia.org/wiki/Deckungsbeitrag

Improvement

Understanding that dollar-based contribution is more effective than standard retail average gross margin % planning “isn’t rocket science” as a cousin recently remarked. Together we created a booklet entitled: “Breakthrough: C&A’s Secret Formula Re-Discovered” and sent it to a number of colleagues and cousins. In the cover letter, he wrote: “we have moved away from the clear commercial thinking of our forefathers. ..I find this interesting and important.”

It pleases me that we have discovered this mistake and things are starting to improve. I hear from old colleagues at C&A that they are once again putting the ideas into practice.

I have also been able to explain the Opportunity Cost and Dollar framework to academics, teachers and top retail executives in the Netherlands through a Master Class at the University of Amsterdam and teaching at the Hoge School Zwolle.

Now a group of a more than a dozen experts including 2 CFOs using input from Professor David E. Bell of Harvard Business School and Dr. Bianca Groen of the University of Amsterdam, has written a paper detailing what I have summarized above. The paper also includes insights from ALDI where decisions were never based on gross margin percentages, but always on Euros. See “Reframing Retail” at www.ProfitperX.com

We have also given “Counting Cash” seminars at C&A Europe to 2 groups of trainees and a class at the Brenninkmeijer Draiflessen center in Mettingen.

It has been interesting to learn what an eye-opener the Opportunity Cost and Dollar Contribution system is for people teaching retail at polytechnics and Universities. Some can’t grasp it all, it is fascinating.

On the other hand, relatively new E-commerce companies are also enlightening because they have also always tracked things at the item level. Some E-commerce companies like Takeaway.com even present gross margin dollars as their top line, that is their actual sales. What C&A calls Sales they refer to as “Gross Merchandise Value (GMV)” and only mention it in footnotes in their reports. Gross merchandise value (GMV) is the combined “Sales” of on the one hand suppliers (Cost Price) and the other hand stores (Gross Margin dollars aka BCP Fund in Euros).

Closing this chapter and moving from Push to Pull

For me personally, it is time to move on. I support my cousins working for Cofra Holding who are a force for good, but I am no longer working for C&A and would like to learn new things.

My goal is no longer to actively try to share these retail insights. They are described in my 2001 Masters thesis (which didn’t include the essential element of Opportunity Cost), a number of other documents, a game, a Youtube video (5 minutes): https://youtu.be/ThM4vwnZFWw a training manual, a booklet, Wikipedia edits, a mobile app, a newspaper article in the Volkskrant and the paper “Reframing Retail” that I have helped create. (My wife jokes that the only thing missing is “Rekenen in Centen in plaats van Procenten; The Musical”).

Now I am moving “from push to pull”. If you want to discuss the ideas feel free to ask me, but I will try not to bring it up if you don’t.

My focus has shifted. Together with www.WarrenBuffett.nl I am setting up a public equity value investing fund to help people increase their wealth by maintaining a margin of safety. Buffett explained the insight and results of value investing in a speech he called “The Superinvestors of Graham- and Doddsville”. Take the time to read it, it is just a few pages. Chances are I also be telling you about Value Machines Fund, using my money-making-machine which spits out Eurocents to help clarify things. Please feel free to reach out to me by email or telephone!

Ansgar John Brenninkmeijer

Amsterdam, Spring 2018

Email: ajb@ValueMachinesFund.nl

Mobile: +31-6-2954768

PS: How could the Brenninkmeijer family be so stupid today? January 2026 "Stupid Brenninkmeijers"

"You do realize that collection building, marginal fulfillment cost, dynamic pricing, timing, and at least ten other factors are also important?

This simplification is useful to drive a very important point about contribution dollars, but that point is also well known and too simple to be the only way to think about retail in a digitally enabled modern omni channel environment. In any event, it is not your responsibility to educate C&A leadership about this, nor to interview C&A executives (current or former).

If you want to teach classes at a university, as I think you already are, then go for it, but as with your other initiatives, please leave the Cofra entities and brands out of it and please make your positive case for your ideas without mentioning them."

Comments, questions or E-mails welcome: ajbrenninkmeijer@gmail.com

No comments:

Post a Comment