March 2009 when the stock market had crashed individual investors were selling: https://www.youtube.com/watch?v=8Sp5lM4ES_I

Dilbert:

Buffett:

"Be fearful when others are greedy, and be greedy when others are fearful."In 1984 Warren Buffett gave a speech and wrote a paper called: The Superinvestors of Graham-and-Doddsville. (Click here voor Dutch Superinvesteerders).

Here are the results of these Superinvestors since 1992 as well as Bestinver, who use the same principals and a Benjamin "Graham" screen started in 2003. At the very bottom are typical results of a mixed portfolio with an average return of about 6% per year.

|

Theory: Mr. Market price <-> Graham Value

SUPERINVESTORS look for values with a significant Margin of Safety relative to stock prices.

HAVE NO FEAR!

Your stock's estimated VALUE is: €

in thousandths of a cent per share at this very second.

Your stock's estimated VALUE is: €

in thousandths of a cent per share at this very second.

Below is a comparision between the Mr. Market price of several Dutch stocks compared to their Graham value (calculated using the Graham Number formula). As well as the Validea.com Benjamin Graham screen criteria with financial numbers from www.iex.nl.

(This doesn't work for financial stocks (as you can see with SNS Reaal in 2007). For companies making heavy losses (such as Ahold around 2002 the Graham value becomes 0.)

SECTOR: [PASS] AHOLD is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. AHOLD's sales of $32,841 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. AHOLD's current ratio €4,804m/€4,171m of 1,2 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for AHOLD is €4,014 million, while the net current assets are €633 million. AHOLD fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. AHOLD's EPS growth over that period passes the EPS growth test.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. AHOLD's E/P of 7% (using the current Earnings) passes this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. AHOLD has a Graham number of √(22,5 x €0,9 EPS x €5,8 Book Value) = €10,8

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. AF's sales of €24,820 million, based on trailing 12 month sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. AF's current ratio of €7,377m/€9,949m of 0.7 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for AF is €9,292 million, while the net current assets are €-2,572 million. AF fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for AF were negative within the last 5 years and therefore the company fails this criterion.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. AFLYY's P/E ratio is not available, the company has no earnings, hence it fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. AF is French and an airline, little wonder that it fails this test.

SECTOR: [PASS] AKZO is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. AKZO's sales of €15,390 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. AKZO's current ratio €7,007m/€5,059m of 1.4 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for AKZO is €3,388 million, while the net current assets are €1,948 million. AKZO fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for AKZO were negative within the last 5 years (2008 and 2012) and therefore the company fails this criterion.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. AKZO's negative E/P (using the current Earnings) fails this test.

|

| 2012 results, 6 Feb. 2013 Market price |

SECTOR: [PASS] Aperam is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Aperam's sales of €3,900 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Aperam's current ratio €716m/€569m of 1.2 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Aperam is €575 million, while the net current assets are €147 million. Aperam fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for Aperam were negative three times within the last 5 years and therefore the company fails this criterion.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. APERAM's negative E/P of -9% (using the current Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Aperam has a Graham number of √(22,5 x €0 EPS x €30 Book Value) = €0

|

| 2012 results, 7 Feb 2013 price |

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. MT's sales of €62,417 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. MT's current ratio €25,121m/€30,958m of 0.8 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for MT is €11,041 million, while the net current assets are $-5,837 million. MT fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. MT's EPS have declined over the past 10 years, and it made a loss in 2012. MT fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. MT's E/P of -14% (using the current Loss) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. MT has a Graham number of √(22,5 x €0,7 EPS x €26 Book Value) = €21

SECTOR: [FAIL] ASML is in the Technology sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published. At that time they were not the driving force of the market as they are today. Although this methodology would avoid ASML, we will provide the rest of the analysis, as we feel times have changed.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. ASML's sales of €4,732 million, based on 2012 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. ASML's current ratio €6,366m/2,086m of 3.1 passes the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for ASML is €1,290 million, while the net current assets are €4,280 million. ASML passes this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for ASML were slightly negative within the last 5 years (2009) and therefore the company fails this criterion.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. ASML's E/P of 5% (using the last 3 years earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. ASML has a Graham number of √(22,5 x €3,3 EPS x €10,71 Book Value) = €28,5

SECTOR: [PASS] Boskalis is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Boskalis' sales of €2,809 million, based on 2011 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Boskalis' current ratio €1,707/€2,021 of 0.8 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Boskalis is €867 million, while the net current assets are €-314 million. Boskalis fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Boskalis' EPS growth was 236% over the past 10 years, Boskalis passes this test.

P/E RATIO: [PASS] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. MT's P/E of 14,3 (using current PE) passes this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Boskalis has a book value of €17 and fails this test.

SECTOR: [PASS] Corio is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Corio's sales of €475 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Corio current ratio €225/€358 of 0.6 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Corio is €3,125 million, while the net current assets are $-133 million. Corio fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Corio's earnings were negative during the past 5 years (2008, 2009) and therefore fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Corio's E/P of 0% (using the last years earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Corio has a Graham number of √(22,5 x €1,6 EPS x €43,13 Book Value) = €40 and passes this test.

SECTOR: [PASS] DE is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. DE's sales of €2,795 million, based on 2012 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. DE's current ratio €1,065m/€1,035m of 3.0 passes the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for DE is €138 million, while the net current assets are €2,248 million. DE passes this test.

LONG-TERM EPS GROWTH: [?] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS figures for DE over 10 years are not available .

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. DE's E/P of 2% (using the last years earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. DE has a Graham number of √(22,5 x €0,4 EPS x €5,3 Book Value) = €6,9 and fails this test.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. DSM's sales of €9,214 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. DSM's current ratio €5,181m/€3,078m of 1.7 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for DSM is €2,640 million, while the net current assets are $2,103 million. DSM fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. DSM's EPS growth of -50% fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. DSM's E/P of 4% (using the last years earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. DSM has a Graham number of √(22,5 x €2,9 EPS x €34,82 Book Value) = €47,8 and passes this test.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Fugro's sales of €2,180 million, based on 2012 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Fugro's current ratio €2,421m/€916m of 2.6 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Fugro is €1,275 million, while the net current assets are €1505 million. Fugro passes this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Fugro's EPS growth was 252% over the past 10 years, Fugro passes this test.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Fugro's E/P of 9% (using the average of last 3 years earnings) passes this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Fugro has a Graham number of √(22,5 x €3,7 EPS x €24,4 Book Value) = €45,4 and passes this test.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. HEINEKEN's sales of €19,893 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. HEINEKEN's current ratio €5537m/€7800m of 0.7 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for HEINEKEN is €15,000 million, while the net current assets are €-2,263 million. HEINEKEN fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. HEINEKEN's EPS growth over that period of 93% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. HEINEKEN's E/P of 5% (using the average over 3 years) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. HEINEKEN has a Graham number of √(22,5 x €3 EPS x €20,30 Book Value) = €37,5 and fails this test.

SECTOR: [FAIL] ING is in the Financial sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published. Although times have changed since then with respect to the risk of financial stocks, several of Graham's criteria, like the Current Ratio and Debt to Current Assets, do not apply to financial companies. As a result, the company will not be able to pass this methodology, although we will include the remainder of the analysis for informational purposes.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. ING's sales of €37,840 million, based on trailing 12 month sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. ING is a financial stock so the current ratio analysis cannot be applied and this criterion cannot be evaluated.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] Long term debt must not exceed net current assets. Companies that meet this criterion display one of the attributes of a financially secure organization. ING is a financial stock so this variable is not applicable and this criterion cannot be evaluated.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for ING were negative within the last 5 years (2008, 2009) and therefore the company fails this criterion.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. ING's E/P of 16% (using the current Earnings) passes this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. ING has a Graham number of √(22,5 x €1,1 EPS x €14,47 Book Value) = €19,2

SECTOR: [PASS] KPN is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. KPN's sales of €13,163 million, based on 2011 sales, passes this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. KPN's current ratio €5,085/€5,609m of 0.9 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for KPN is $13,010 million, while the net current assets are $-524 million. KPN fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for KPN have decreased since 2003 and therefore the company fails this criterion.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. KPN's E/P of 19% (using the current Earnings) passes this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. KPN has a Graham number of √(22,5 x €0,9 EPS x €2 Book Value) = €6,2

SECTOR: [PASS] Philips is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Philips' sales of €24,800 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Philips' current ratio €12,528m/€9,955 of 1.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Philips is €7,950 million, while the net current assets are €2,573 million. Philips fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for Philips were negative within the last 5 years (2008, 2011) and therefore the company fails this criterion.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. Philips' P/E of 89,4 (using the current PE) fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Phlilps has a book value of €12,18 and fails this test.

SECTOR: [PASS] PNL is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. PNL's sales of €4,350 million, based on 2011 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. PNL's current ratio €2,528m/€1,204m of 2.1 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for PNL is €1,607 million, while the net current assets are €-1,204 million. PNL fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. EPS for PNL have declined over the last 10 years and therefore the company fails this criterion.

P/E RATIO: [PASS] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. PNL's P/E of 4,2 (using the current PE) passes this test.

PRICE/BOOK RATIO: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. PNL has a book value of €1 and passes this test.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Randstad's sales of €17,087 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Randstad's current ratio €3,114m/€3,948m of 0.8 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Randstad is €59 million, while the net current assets are €-834 million. Randstad fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Randstad's EPS growth was 186% over the past 10 years, Randstad passes this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Randstad's E/P of 3% (using the last 3 years Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Randstad has a Graham number of √(22,5 x €0,8 EPS x €17 Book Value) = €18

SECTOR: [PASS] REN is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. REN's sales of €6,902 million, based on 2011 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. REN's current ratio €3,111m/€5,262m of 0.6 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for REN is €5,754 million, while the net current assets are €-2,151 million. REN fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. REN's EPS growth over that period of 324% passes the EPS growth test.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. REN's P/E of 16.7 (using the last 3 year's PE) fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. REN has a book value of €2,3 per share and fails this test.

Shell includes 2012 results 31/1/2012

SECTOR: [PASS] RDS.A is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. RDS.A's sales of €346,244 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. RDS.A's current ratio €85,038m/€69,491m of 1.2 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for RDS.A is €25,271 million, while the net

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. RDS.A's EPS growth over that period of 124% passes the EPS growth test.

P/E RATIO [PASS] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. RDS.A's P/E of 8.30 (using the 3 year PE) passes this test.

PRICE/BOOK RATIO: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. RDS.A has a book value of €22,31 per share and passes this test.

Margin of Safety: A €41 Graham value for sale at a €25,84 Mr. Market price => You can buy €1 euro of value for 63 cents.

SECTOR: [PASS] SBM is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. SBM's sales of €2,836 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. SBM's current ratio €2,208m/€1,934m of 1.1 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for SBM is €1,414 million, while the net current assets are €274 million. SBM fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. SBM's EPS were negative in 2011 and 2012 therefore SBM fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. SBM's E/P of 0% (using the current Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. SBM has a Graham number of √(22,5 x €0,5 EPS x 6,32 Book Value) = €8,6

TNT problem: No numbers before 2011.

SECTOR: [PASS] TNT is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. TNT's sales of €7,316 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. TNT's current ratio €1,902m/€1,329m of 1.4 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for TNT is €225 million, while the net current assets are €573 million. TNT passes this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. TNT's EPS were negative in 2011 and 2012 therefore TNT fails this test.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. TNT's P/E can't be calculated (using last 3 year's PE), therefore TNT fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. TNT has a Graham number of √(22,5 x €0,1 EPS x €5 Book Value) = €2,8 and fails this test.

SECTOR: [PASS] UN is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. UN's sales of €51,324 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. UN's current ratio €12,147m/€15,815m of 0.8 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for UN is €14,635 million, while the net current assets are €-3,668 million. UN fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. UN's EPS growth over that period of 139% passes the EPS growth test.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. UN's P/E of 20 (using last 3 year's PE) fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. UN has a book value of €5,20 per share, and fails this test.

SECTOR: [PASS] WKL is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. WKL's sales of €3,354 million, based on 2011 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. WKL's current ratio €1,586m/€2,47m of 0.6 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for WKL is €2,591 million, while the net current assets are €-871 million. UN fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. WKL's EPS have declined over the past 5 years, WKL fails the EPS growth test.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. WKL's P/E of 21 (using last 3 year's PE) fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. UN has a book value of €5,20 per share, and fails this test.

SECTOR: [PASS] Aalberts is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Aalberts' sales of €2,025 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Aalberts' current ratio €663m/€605m of 1.1 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Aalberts is €362 million, while the net current assets are €58 million. Aalberts fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Aalberts' EPS growth over that period of 175% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Aalberts's E/P of 6% (using the average of last 3 years) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Aalberts has a Graham number of √(22,5 x €1,3 EPS x €8,9 Book Value) = €16,8

Advanced Metallurgical Group

SECTOR: [PASS] AMG is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. AMG's sales of €995 million, based on 2011 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. AMG's current ratio €440m/€217m of 2.0 passes the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for AMG is €169 million, while the net current assets are €223 million. AMG passes this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. AMG's EPS were negative in 2009, AMG fails this test.

P/E RATIO: [FAIL] The Price/Earnings (P/E) ratio, based on the greater of the current PE or the PE using average earnings over the last 3 fiscal years, must be "moderate", which this methodology states is not greater than 15. Stocks with moderate P/Es are more defensive by nature. AMG's P/E of 52 (using the current PE) fails this test.

PRICE/BOOK RATIO: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. AMG has a book value of €5,77, but fails this test.

ASMI

BAM

BAM

SECTOR: [FAIL] Binck is in the Financial sector, which is one sector that this methodology avoids. Technology and financial stocks are considered too risky to invest in. Several of Graham's criteria, like the Current Ratio and Debt to Current Assets, do not apply to financial companies. As a result, the company will not be able to pass this methodology, although we will include the remainder of the analysis for informational purposes.

SALES: [FAIL] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Binck's sales of €160 million, based on 2012 sales, fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Binck's EPS growth over that period of 210% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Binck's E/P of 4% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Binck has a Graham number of √(22,5 x €0,4 EPS x 6,11 Book Value) = €7,7

Brunel old

BRUNEL new

CSM

Delta Lloyd: Financial, doesn't work in Graham value. Not enough years figures either. Losses in past 5 years: fail.

Heijmans

Heijmans

Imtech 2012 numbers were expected February 5th, now they are delayed.

2011 Imtech Graham screen: FAILED in CURRENT RATIO and LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS. Which is the reason they are now in trouble with the banks after a major loss in Poland.

Book value 2011 was €932m/87,5m shares is €10,6 per share. The loss in Poland is at least €100million. Too be safe, we'll make it 232m. Guesstimate book value per share = €700/€87,5 = €8,-

New lower EPS estimate for 2013 €1,30 (was €1,7 in 2011). €0,- for 2012.

Guesstimate of Graham value: Graham number of √(22,5 x €1,3 EPS x 8 Book Value) = €15,2

Imtech 2012 numbers February 5th

Mediq: When price was at around €8,50 in 2012, Advent offered to buy Mediq, shareholders said the €13,25 offer was too low, it will be taken over in 2013 for €14.

Nieuwe Steen Investments

Nieuwe Steen Investments

SECTOR: [PASS] NSI is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [FAIL] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. NSI's sales of €160 million, based on 2012 sales, fails this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. NSI's current ratio €99m/€316m of 0.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for NSI is €1,042 million, while the net current assets are €-217 million. NSI fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. NSI made a loss in 2009 and 2012 and therefore fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. NSI's E/P of 0% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. NSI has a Graham number of √(22,5 x €0,7 EPS x €9,78 Book Value) = €12,7

SECTOR: [PASS] Nutreco is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Nutreco's sales of €5,229 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Nutreco's current ratio €1,701m/€1,315m of 1.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Nutreco is €494 million, while the net current assets are €386 million. Nutreco fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Nutreco's EPS growth since 2008 of 53% passes the EPS growth test.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Nutreco's E/P of 7% (using the current Earnings) passes this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Nutreco has a Graham number of √(22,5 x €4,9 EPS x €28,09 Book Value) = €57,3

SECTOR: [FAIL] SNS is in the Financial sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published. Several of Graham's criteria, like the Current Ratio and Debt to Current Assets, do not apply to financial companies. As a result, the company will not be able to pass this methodology.

SNS Reaal: The bank was nationalized (because of impending bankruptcy) February 1st 2013. Shareholders received €0,00.

Ten Cate old

Chart above before 2012 results, chart below with 2012 results.

Ten Cate new

SECTOR: [PASS] Ten Cate is neither a technology nor financial Company, and therefore this methodology is applicable.

SECTOR: [PASS] Ten Cate is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Ten Cate's sales of €1049 million, based on 2012 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Ten Cate's current ratio €413m/€179m of 2.3 passes the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Ten Cate is €280 million, while the net current assets are €234 million. Ten Cate fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Ten Cate's EPS growth over that period of 23% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Ten Cate's E/P of 5% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Ten Cate has a Graham number of √(22,5 x €1,7 EPS x 17,25 Book Value) = €26

SECTOR: [FAIL] TomTom is in the Technology sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. TomTom's sales of €1057 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. TomTom's current ratio €477m/€442m of 1.1 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for TomTom is €362 million, while the net current assets are €35 million. TomTom fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. TomTom made losses in 2008 and 2011 and therefore fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. TomTom's E/P of -9% (using the past 3 years Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. TomTom has a Graham number of √(22,5 x €0,1 EPS x €3,76 Book Value) = €3,1

Unit 4

SECTOR: [PASS] Accell is neither a technology nor financial Company, and therefore this methodology is applicable.

SECTOR: [FAIL] Binck is in the Financial sector, which is one sector that this methodology avoids. Technology and financial stocks are considered too risky to invest in. Several of Graham's criteria, like the Current Ratio and Debt to Current Assets, do not apply to financial companies. As a result, the company will not be able to pass this methodology, although we will include the remainder of the analysis for informational purposes.

SALES: [FAIL] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Binck's sales of €160 million, based on 2012 sales, fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Binck's EPS growth over that period of 210% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Binck's E/P of 4% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Binck has a Graham number of √(22,5 x €0,4 EPS x 6,11 Book Value) = €7,7

Brunel old

CSM

Delta Lloyd: Financial, doesn't work in Graham value. Not enough years figures either. Losses in past 5 years: fail.

|

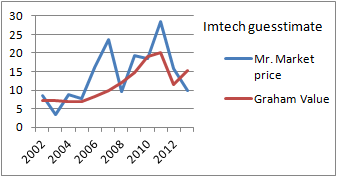

| Chart February 1st 2013 |

2011 Imtech Graham screen: FAILED in CURRENT RATIO and LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS. Which is the reason they are now in trouble with the banks after a major loss in Poland.

Book value 2011 was €932m/87,5m shares is €10,6 per share. The loss in Poland is at least €100million. Too be safe, we'll make it 232m. Guesstimate book value per share = €700/€87,5 = €8,-

New lower EPS estimate for 2013 €1,30 (was €1,7 in 2011). €0,- for 2012.

Guesstimate of Graham value: Graham number of √(22,5 x €1,3 EPS x 8 Book Value) = €15,2

|

| Imtech guesstimate with 300 million Polish write off and 0.- profit in 2012 (February 4th, 2013) |

Imtech 2012 numbers February 5th

Mediq: When price was at around €8,50 in 2012, Advent offered to buy Mediq, shareholders said the €13,25 offer was too low, it will be taken over in 2013 for €14.

SECTOR: [PASS] NSI is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [FAIL] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. NSI's sales of €160 million, based on 2012 sales, fails this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. NSI's current ratio €99m/€316m of 0.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for NSI is €1,042 million, while the net current assets are €-217 million. NSI fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. NSI made a loss in 2009 and 2012 and therefore fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. NSI's E/P of 0% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. NSI has a Graham number of √(22,5 x €0,7 EPS x €9,78 Book Value) = €12,7

SECTOR: [PASS] Nutreco is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Nutreco's sales of €5,229 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Nutreco's current ratio €1,701m/€1,315m of 1.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Nutreco is €494 million, while the net current assets are €386 million. Nutreco fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Nutreco's EPS growth since 2008 of 53% passes the EPS growth test.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Nutreco's E/P of 7% (using the current Earnings) passes this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Nutreco has a Graham number of √(22,5 x €4,9 EPS x €28,09 Book Value) = €57,3

SECTOR: [FAIL] SNS is in the Financial sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published. Several of Graham's criteria, like the Current Ratio and Debt to Current Assets, do not apply to financial companies. As a result, the company will not be able to pass this methodology.

SNS Reaal: The bank was nationalized (because of impending bankruptcy) February 1st 2013. Shareholders received €0,00.

Ten Cate old

Chart above before 2012 results, chart below with 2012 results.

Ten Cate new

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Ten Cate's sales of €1049 million, based on 2012 sales, pass this test.

CURRENT RATIO: [PASS] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Ten Cate's current ratio €413m/€179m of 2.3 passes the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Ten Cate is €280 million, while the net current assets are €234 million. Ten Cate fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Ten Cate's EPS growth over that period of 23% passes the EPS growth test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Ten Cate's E/P of 5% (using the current Earnings) fails this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Ten Cate has a Graham number of √(22,5 x €1,7 EPS x 17,25 Book Value) = €26

SECTOR: [FAIL] TomTom is in the Technology sector, which is one sector that this methodology avoids. Technology and financial stocks were considered too risky to invest in when this methodology was published.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. TomTom's sales of €1057 million, based on 2012 sales, pass this test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for TomTom is €362 million, while the net current assets are €35 million. TomTom fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. TomTom made losses in 2008 and 2011 and therefore fails this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. TomTom's E/P of -9% (using the past 3 years Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. TomTom has a Graham number of √(22,5 x €0,1 EPS x €3,76 Book Value) = €3,1

Unit 4

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Acell's sales of €772 million, based on 2012 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Accell's current ratio €408m/€305m of 1.3 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Accell is €15,8 million, while the net current assets are €103 million. Accell passes this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Accell's EPS growth over that period of 266% passes the EPS growth test.

Earnings Yield: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Accell's E/P of 8% (using the current Earnings) passes this test.

Graham Number value: [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Accell has a Graham number of √(22,5 x €1,4 EPS x €10,4 Book Value) = €18,5

Margin of Safety: A €18,5 Graham value for sale at a €13,2 Mr. Market price. You can buy €1 euro of value for 70 cents.

Arseus

Source of inputs: iex.nl

Results:

Comments, questions or E-mails welcome: ajbrenninkmeijer (a) gmail.com

5 comments:

Dear John,

fun to see you developping a genuine feeling for Value Investing. No other than real life, it comes in many shapes and sizes. Good luck and I hope to stay helpfull during your journey.

Bedankt voor je tips !

Samen Is Niet Alleen, Altijd Samen :)

Mooie site Ansgar ;) mooie samenvatting value investing, ben benieuwd naar toekomstige updates

It provides comprehensive knowledge of the subject. Everything written in this blog is close to satisfactory level. I am sure no one can raise any issue about all the information delivered here.cursus medium

Post a Comment