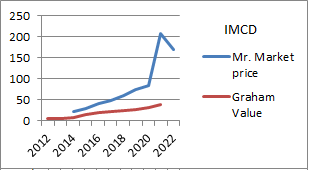

IMCD's share price has decreased by about a fifth from the all-time high last year. Depending on how you look at it, the share price still seems high compared to the Benjamin Graham Defensive value:

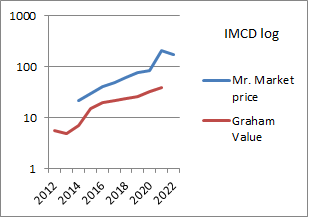

When making charts (of 15x Earmings per Share and Price) Peter Lynch used a logarithmic scale which shows relative differences better than a normal scale:

As Warren Buffett says: "It is far better to invest in a wonderful company at a fair price, then a fair company at a wonderful price."

SECTOR: [PASS] IMCD is neither a technology nor financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. IMCD's sales of €3 380 million, based on 2021 sales, pass this test. Sales have increased significantly in the past years.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. IMCD's current ratio €1 004m/€713m of 1.4 fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for IMCD is €738 million, while the net current assets are €291 million. IMCD fails this test.

LONG-TERM EPS GROWTH:[PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. IMCD's EPS have grown by over 100% and pass this test.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. IMCD's E/P of 2% (using this years estimated earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. IMCD has a Graham number of √(15 x €2,8 EPS x 1,5 x €23 Book Value) = €39 and fails this test.

Dividend: 1,02 EUR / 168 EUR = 0,6% and increasing.

The company is doing well, the stock seems to have been priced to perfection. Not for the defensive investor above EUR 50.

No comments:

Post a Comment