|

| LOG scale |

Alibaba Graham Defensive Analysis:

SECTOR: [PASS][FAIL] Alibaba is neither dependant on one niche technology nor a financial Company, and therefore this methodology is applicable.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Alibaba's sales of $110,000 million, based on 2021 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Alibaba's current ratio $98 000m/€60 000m of 1.6 just fails the test.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [PASS] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that meet this criterion display one of the attributes of a financially secure organization. The long-term debt for Alibaba's is $21 000 million, while the net current assets are $38 000 million. Alibaba fails this test.

LONG-TERM EPS GROWTH: [PASS] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Alibaba's EPS growth over that period of 2 300% easily passes the EPS growth test.

EARNINGS YIELD: [PASS] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Alibaba's E/P of 6.5% (using the average of last 3 years) passes this test.

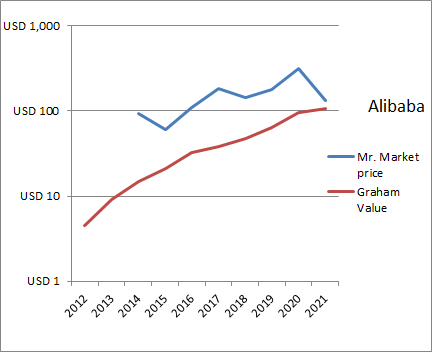

GRAHAM NUMBER VALUE: [FAIL] [PASS] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Alibaba has a Graham number of √(15 x $7 EPS x 1,5 x $55 Book Value) = €105 is almost equal to share price

Dividend: Alibaba does not pay a dividend, but is buying back shares.

Conclusion: January 2022 at 130 USD: Alibaba is hoping to grow revenue by more than 20% this year and expand to 2 billion customers. Seems like a buy for a growth investors and almost for a Graham Defensive Investor. A buy for an intelligent investor. There is China country risk.

Disclaimer: I own Alibaba shares via www.valuemachinesfund.nl

No comments:

Post a Comment